You have been investing in ELSS funds for the Section 80C deduction and watching the portfolio grow. Now you need liquidity and wonder whether those tax-saving units can serve as collateral. The answer turns on one thing: how long each batch of units has been held.

What Is ELSS and Why It Has a Lock-In Period?

ELSS (Equity Linked Savings Scheme) is a category of equity mutual fund that qualifies for a tax deduction of up to Rs 1.5 lakh per year under Section 80C of the Income Tax Act. In exchange for this benefit, each unit carries a mandatory 3-year lock-in from its investment date.

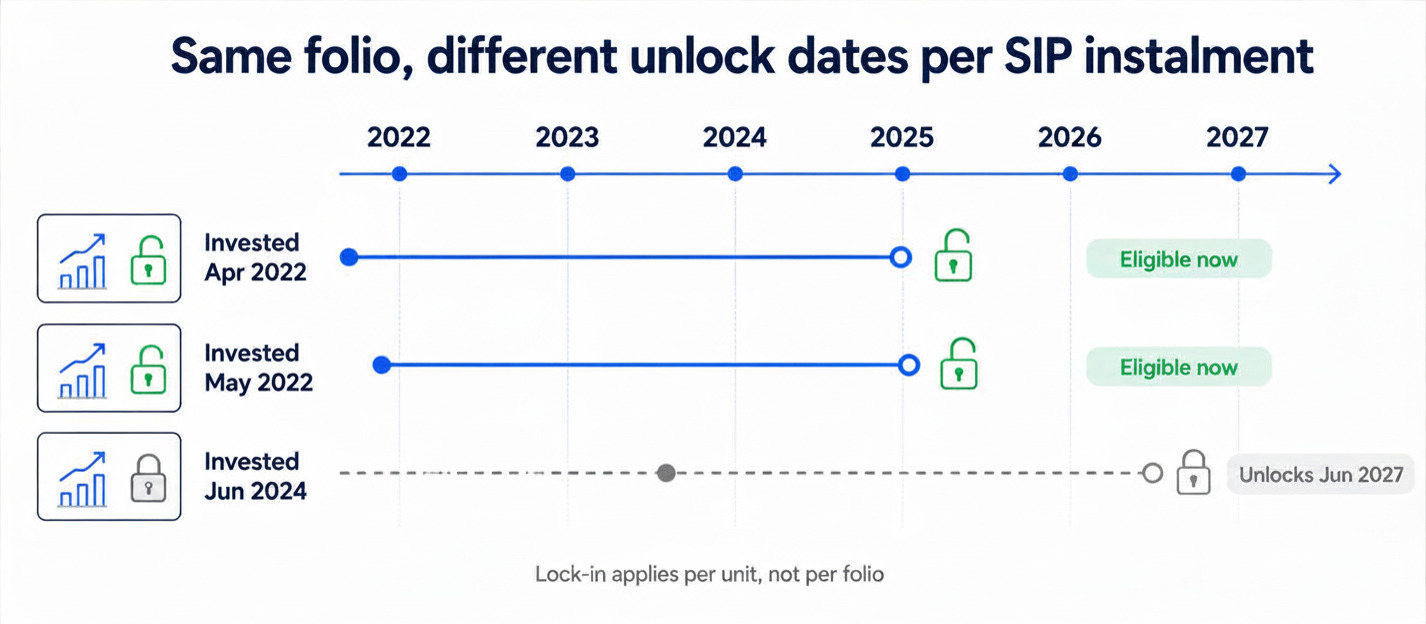

The lock-in is per unit, not per folio. Monthly SIP investors have batches of units with different unlock dates: an April 2022 instalment unlocks in April 2025, a May 2022 instalment in May 2025, and so on. At any given point, your ELSS folio may contain a mix of locked and unlocked units.

Can You Get a Loan Against ELSS Mutual Funds?

Check your credit limit on Volt Money. Free, takes 15 seconds.

Check your limit →Not during the lock-in period. ELSS units under the 3-year restriction cannot be pledged as collateral. Lenders and RTAs (CAMS, KFintech) will reject lien marking requests on locked units. There is no workaround, regardless of the lender or platform.

Once the 3-year period is complete for a specific batch of units, those units become eligible for pledging, subject to the lender's approved securities list. From the lender's perspective, post-lock-in ELSS units are treated the same as any other equity mutual fund — 70% LTV, no credit score requirement.

For SIP investors, only units with investment dates more than 3 years ago are pledgeable. The rest remain locked. When you check eligibility on Volt Money, the platform automatically filters out locked ELSS units and shows only your currently pledgeable holdings.

What Happens After the 3-Year Lock-In Ends?

Once the lock-in expires on a batch of ELSS units, those units become standard equity fund units with no further restriction. You can redeem them, hold them, switch them, or pledge them for a loan.

Pledging post-lock-in ELSS units works identically to pledging any equity fund. The lender checks the scheme against their approved list, marks a lien on the eligible units, and sets a credit limit of up to 70% of the current NAV. The units keep compounding. The LTCG tax clock continues running from the original investment date, not from the pledge date.

Alternatives to Borrowing Against ELSS During the Lock-In

If your ELSS units are still locked and you need liquidity now, there are practical options:

- Pledge your non-ELSS portfolio: Most investors hold a mix of ELSS and non-ELSS funds. Liquid, debt, large-cap equity, or hybrid funds are likely eligible to pledge even while your ELSS units are locked. A credit limit against those holdings can cover your immediate need without waiting.

- Bridge with a short-term loan: If the ELSS units are close to unlocking (within 3 to 6 months) and you need a modest amount, a short-term personal loan can bridge the gap. Repay it once the units unlock.

What you cannot do: redeem locked ELSS units early, regardless of urgency. The 3-year restriction is statutory and enforced at the RTA level. No lender, platform, or workaround can override it.

Tax Implications of Pledging ELSS Units

Pledging ELSS units does not affect your Section 80C deduction. The tax benefit was claimed in the year of investment and is not reversed or adjusted by what you do with the units afterward.

Pledging also does not trigger a capital gains event. No redemption has occurred. The units remain in your name and are still considered held for tax purposes. The LTCG clock continues from the original investment date.

If you eventually redeem post-lock-in ELSS units after using them as collateral, the gain is calculated from the original investment date to the redemption date. Since all post-lock-in ELSS units have been held for at least 3 years, they automatically qualify for LTCG treatment at 12.5% above the Rs 1.25 lakh annual exemption.

For a full overview of how LAMF works across fund types, see What Is a Loan Against Mutual Funds.