You have Rs 20 lakh sitting in mutual funds and suddenly need Rs 5 lakh — for a medical bill, a business shortfall, or a renovation that can't wait. The obvious moves feel like selling your funds, or taking an expensive personal loan at 14–30% p.a. But redeeming those units triggers capital gains tax, breaks years of compounding, and permanently exits positions you built patiently. Redeeming mutual funds typically takes 2–5 business days to reach your bank account. A credit facility through Volt Money is available in under 10 minutes.

A loan against mutual funds (LAMF) lets you borrow against your portfolio without selling a single unit, at rates starting from 9.99% p.a., with money in your account in as little as 10 minutes*.

What Is a Loan Against Mutual Funds (LAMF)?

LAMF is a secured credit facility where your mutual fund units serve as collateral. The lender places a lien on your pledged units — a process called lien marking — and gives you a credit limit you can draw from as needed. You pay interest only on the amount you actually withdraw, not on the total limit sanctioned.

For example: you have Rs 10 lakh in mutual funds. The lender marks a lien on those units — a digital flag that prevents them from being sold — and gives you a credit limit of up to Rs 7 lakh. You withdraw Rs 2 lakh to cover your expense and pay interest only on those Rs 2 lakh. Your entire Rs 10 lakh stays invested and continues to grow in the market.

Think of it as a credit limit backed by your portfolio rather than your income. Your funds stay invested throughout the loan period, continuing to earn returns while you have access to the cash you need. Loan amounts range from Rs 10,000 to Rs 5 crore depending on your portfolio size and lender.

LAMF is offered by banks, NBFCs, and fintech platforms. Banks may tie the product to an existing relationship or require branch paperwork. Fintech platforms like Volt Money have simplified the process significantly — you can go from an eligibility check to a live credit limit in a single session, entirely online, in under 10 minutes.

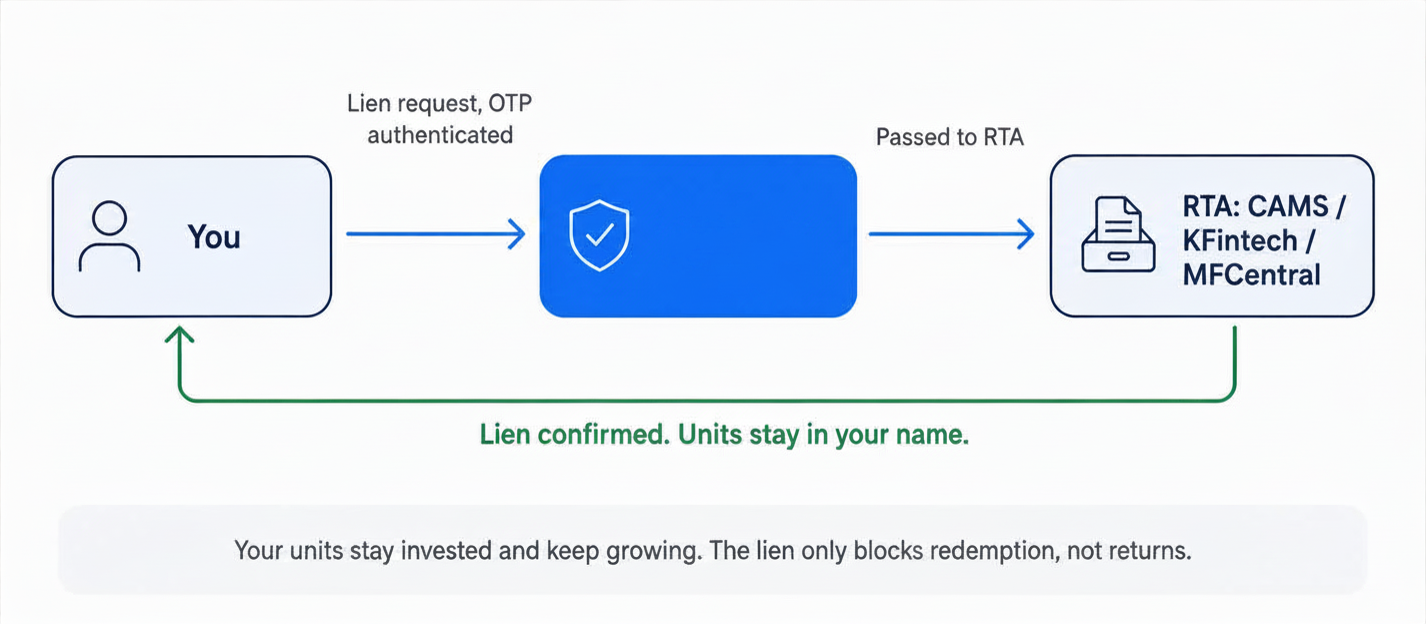

How LAMF Works: The Pledge and Lien Process

Check your credit limit on Volt Money. Free, takes 15 seconds.

Check your limit →

Three parties are involved: you (the borrower), the lender, and the registrar and transfer agent (RTA) that maintains unit-level records of your mutual fund holdings.

When you apply for a credit limit and select the units you want to pledge, the lender sends a lien marking request to the RTA responsible for those fund houses. In India, the major RTAs are CAMS (serving HDFC MF, ICICI Prudential, SBI MF, Nippon India, and others) and KFintech (serving Aditya Birla Sun Life, UTI MF, Franklin Templeton, and others). MFCentral is an integrated platform connecting both.

The RTA marks a lien on the specified units. The units remain in your name and stay invested, but you cannot redeem or switch them while the lien is active. Once lien marking is confirmed, the lender calculates your credit limit and your credit facility goes live. Interest accrues daily on the withdrawn balance only. Every rupee you repay restores the credit facility immediately.

The entire process is OTP-authenticated. No physical signatures. No paperwork to courier.

Who Is Eligible for LAMF?

Most Indian mutual fund investors qualify. The standard criteria across lenders are:

- Indian resident, 18 years or above.

- Mutual fund units on the lender's approved securities list.

- Portfolio value above the minimum pledgeable threshold (starting from as low as Rs 15,000).

No minimum credit score required. Volt Money's lending partner checks your credit score as part of the process, but no minimum score is required for availing LAMF. Your portfolio is the only security that matters.

That last point matters more than most people realise. A self-employed professional or business owner with a 600 CIBIL score who holds Rs 10 lakh in equity funds can get a credit limit where they might be rejected, or charged a premium, on a personal loan. Even someone with no credit score at all can access LAMF — no minimum credit score is required for availing LAMF.

Interest Rates, LTV Ratios, and Charges

LAMF interest rates start at 9.99% p.a. and typically go up to 12% p.a. depending on the lender's policy. Compared to personal loan rates of 14% to 30%, the savings on a Rs 5 lakh, 90-day borrow can exceed Rs 10,000.

The loan-to-value (LTV) ratio determines how much you can borrow as a percentage of your pledged portfolio's current fund value:

- Equity and hybrid mutual funds: up to 70% LTV (highest in industry)

- Debt mutual funds (liquid, short duration, gilt): up to 85% LTV

- Hybrid mutual funds: 50% to 65% LTV depending on equity-debt composition

So if you pledge equity funds worth Rs 10 lakh, your maximum credit limit is Rs 7 lakh. Pledge liquid funds worth Rs 10 lakh and you access up to Rs 8.5 lakh. Because the credit limit is tied to current fund value, it adjusts as portfolio values change. Your exact limit appears within seconds of entering your PAN at the start of the application.

Processing fees are 0.5% to 1% of the credit limit (minimum Rs 999), charged once at setup. Prepayment charges generally do not apply — you repay whenever you have the funds.

Should You Sell Your Mutual Funds or Take LAMF?

Selling has costs that don't show up as a fee on your statement. Redeeming equity funds held for more than 12 months triggers LTCG tax at 12.5% on gains above the Rs 1.25 lakh annual exemption. Funds held under 12 months attract STCG at 20%. Add the exit load (usually 1% if redeemed within a year) and the compounding you lose by exiting early, and the picture changes significantly.

For most investors with equity funds showing meaningful gains, borrowing at 9.99% p.a. for a short period costs less than selling and paying 12.5% to 20% on the gains. Your funds remain invested throughout and continue to grow — the lien only restricts redemption, not performance.

Which Mutual Funds Are Eligible for LAMF?

Most fund categories qualify with a few key exceptions:

- Equity funds: large-cap, mid-cap, small-cap, flexi-cap, index funds, most sectoral and thematic funds

- Debt funds: liquid, overnight, ultra-short duration, short duration, banking and PSU, gilt

- Hybrid funds: balanced advantage, aggressive hybrid, equity savings, and conservative hybrid

- ETFs and fund-of-funds, subject to the lender's approved list

Not eligible: ELSS funds during the 3-year lock-in period, closed-end funds within their restriction period, and any scheme not on the lender's approved securities list. Once the ELSS lock-in expires, those units become eligible like any other equity fund.

How to Apply for LAMF on Volt Money

The application is entirely online and typically takes under 10 minutes from start to fund disbursal:

- Enter your PAN on Volt Money. The platform scans your portfolio and shows your eligible credit limit in about 15 seconds.

- Complete a simple OTP-based KYC using DigiLocker. You will need your Aadhaar-linked mobile number. This takes under 2 minutes.

- Add your bank account details. This is the account to which withdrawals will be credited and from which monthly interest and repayments will be debited.

- Pledge your funds with a single OTP. Volt Money coordinates the lien marking request with CAMS, KFintech, or MFCentral across all fund houses in one step.

- Review and accept the loan agreement digitally. No physical signature needed.

- Withdraw any amount up to your limit directly to your bank account.

For the complete step-by-step walkthrough including what to check in the loan agreement and how lien release works, see How to Take a Loan Against Mutual Funds.

Risks of LAMF: When It Does Not Make Sense

LAMF is well-suited for short-to-medium-term needs, but it carries a few risks:

- Margin call risk: If NAV drops sharply and pushes your LTV above the threshold, the lender can ask you to pledge more units or repay part of the balance. Equity-backed LAMF carries higher margin call risk than debt-backed. For example: if you pledged equity funds worth Rs 10 lakh at 70% LTV (credit limit of Rs 7 lakh) and the NAV falls to Rs 8 lakh, your outstanding loan now represents more than 70% of the current fund value. The lender will ask you to pledge additional units or repay part of the balance.

- Interest accumulation over the tenure: The credit facility runs for up to 6 years. There is no forced monthly principal repayment, so if you only pay the monthly interest without reducing the principal, costs accumulate. Set a repayment plan before drawing.

- Lien locks redemption: Pledged units cannot be redeemed even in an emergency. Keep some portfolio unpledged as a liquid reserve. On Volt Money, you can request unpledging in under 10 minutes from the app.