You know why a loan against mutual funds makes sense. The part that trips people up is what actually happens after you click apply: what lien marking does to your units, what to expect across different fund houses, and how repayment on a credit facility works in practice. This guide covers every step.

Before You Begin: What You Need Ready

Collecting these before you start prevents mid-application delays:

- PAN number, to identify your mutual fund portfolio automatically.

- Aadhaar-linked mobile number, required for OTP-based lien marking and KYC through DigiLocker.

- Bank account details, for fund disbursal and automatic interest debits.

No physical documents, printed forms, or branch visit required at any stage. If you haven't yet decided whether LAMF suits your situation, start with What Is a Loan Against Mutual Funds for a full overview of costs, eligibility, and how it compares to selling your portfolio.

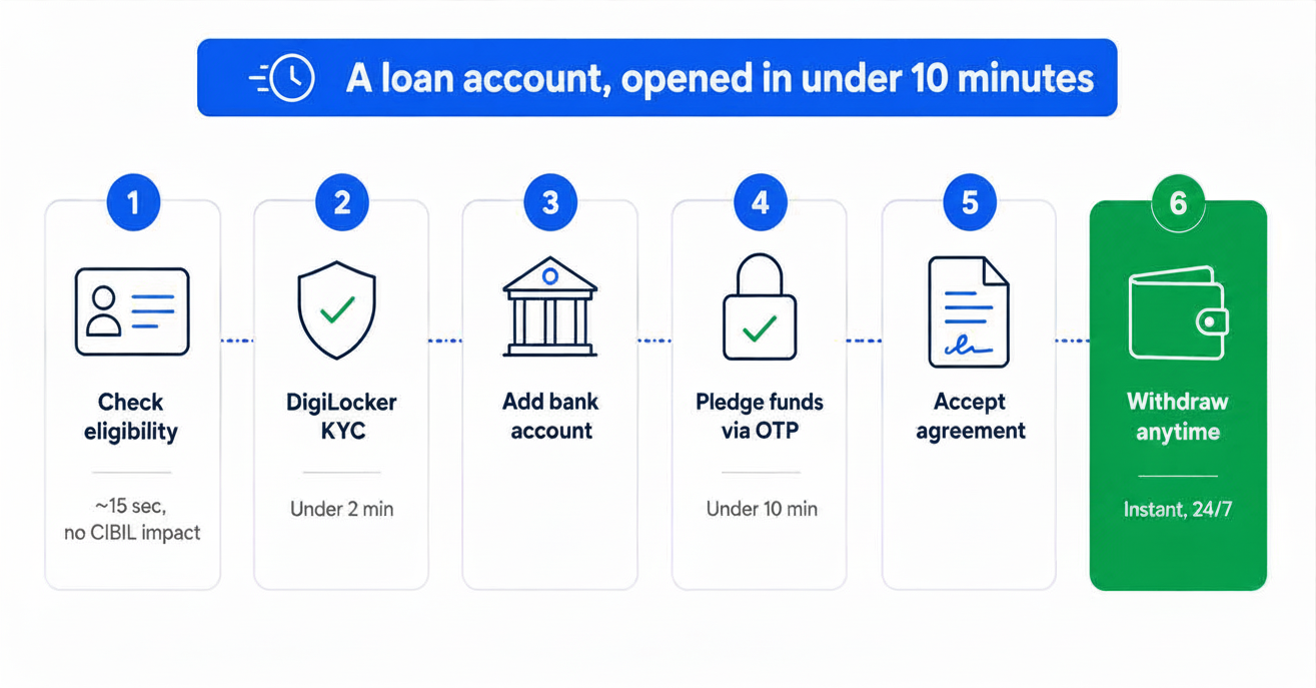

Step 1: Check Your Eligibility and Credit Limit

Check your credit limit on Volt Money. Free, takes 15 seconds.

Check your limit →

Visit the Volt Money eligibility check page, enter your PAN, and the platform scans your mutual fund portfolio against the lender's approved securities list automatically. Within about 15 seconds, you will see which funds are eligible to pledge, your maximum credit limit, and the interest rate that applies.

If you hold funds across multiple fund houses — say Axis, HDFC, and Mirae Asset — they all appear in a single scan. You choose which eligible funds to pledge. You don't have to pledge everything: pledge only what's needed to support the credit limit you want.

Step 2: Complete Your KYC

Volt Money's lending partner uses a simple OTP-based DigiLocker KYC to verify your identity. You will receive an OTP on your Aadhaar-linked mobile number. The KYC process is entirely digital and takes under 2 minutes — no documents to upload or scan.

Step 3: Add Your Bank Account Details

Link the bank account to which withdrawals will be credited and from which monthly interest and loan repayments will be debited. This account is tied to your credit facility for all transactions throughout the 6-year tenure.

Step 4: Pledge Your Mutual Fund Units (Lien Marking Explained)

When you pledge units, you instruct the fund's registrar and transfer agent (RTA) to place a lien on those specific units. A lien means the units cannot be redeemed, switched, or transferred while the restriction is active. They remain in your name, keep earning returns, and can be released any time you choose via the Volt app in under 10 minutes.

The major RTAs in India are CAMS and KFintech. MFCentral connects both. When you authorise the pledge on Volt Money, the platform sends the lien request to the correct RTA on your behalf. You confirm the instruction via OTP on your Aadhaar-registered mobile number. Lien marking typically completes within 10 minutes.

For the detailed mechanics of how lien marking works, how to check which units are marked, and how the lien is released, see What Is Lien Marking on Mutual Funds.

Step 5: Review and Sign Your Loan Agreement

After lien marking is confirmed, you receive the loan agreement and Key Fact Statement (KFS) for review. Before signing, focus on two clauses specifically:

- The margin call clause — what the lender is permitted to do if the NAV of your pledged units falls below the minimum required LTV (typically sell enough units to restore the ratio).

- The interest debit schedule — when the monthly interest charge is auto-debited from your linked bank account.

Review and accept the loan agreement digitally. No physical signature or printout needed. The agreement is legally valid under the Information Technology Act.

Step 6: Withdraw Funds as Needed

Once your credit facility is live, transfer any amount up to your limit to your linked bank account at any time. This is where LAMF behaves very differently from a personal loan.

You do not take the full credit limit upfront. If you need Rs 2 lakh today and possibly another Rs 1 lakh in six weeks, draw Rs 2 lakh now. Interest accrues from the withdrawal date on the drawn amount only. The second draw can happen later without a new application, at the same rate, from the same credit facility.

There is no fixed repayment schedule. You have up to 6 years to repay the principal. Pay the monthly interest debit automatically and repay the principal whenever you have surplus funds. Every rupee you repay restores your available credit facility immediately.

How Lien Release Works When You Repay

Because LAMF works as a credit facility, the lien on your pledged units remains active even after you repay. This allows you to withdraw again any time during your 6-year tenure without re-pledging. When you want to fully exit the credit facility, request unpledging directly from the Volt app or website. Unpledging typically completes in under 10 minutes.

If you repay only part of the outstanding balance, the lien remains on your full pledged holding. The lender does not automatically release units on partial repayment. To release pledged units, request unpledging through the Volt app once your outstanding balance allows it.

Risks to Know Before You Apply

Margin call risk is the one to watch. If the NAV of your pledged funds falls significantly, the lender will ask you to top up collateral or repay part of the balance. Keep a buffer: don't draw the full credit limit, so a market dip doesn't immediately trigger a margin call.