Most investors searching for a loan against mutual funds picture something like a personal loan: a fixed amount, repaid in EMIs over a set tenure. What they actually get in most cases is a flexi facility. That difference changes the cost significantly. Personal loans for the same amount typically carry interest rates of 14% to 30% p.a., making the credit facility against mutual funds a far cheaper alternative. This article covers how the loan against mutual fund structure works, how interest is calculated to the day, and when it is the cheaper choice.

What Is Flexi Loan Against Mutual Funds?

A Loan Against Mutual Funds (LAMF) is a credit facility secured by your pledged mutual fund units. You receive a sanctioned credit limit based on the current NAV and the loan-to-value (LTV) ratio of your pledged portfolio. You can draw any amount up to that limit at any time and pay interest only on the amount you actually withdraw, not on the entire sanctioned limit. Depending on the fund type, your sanctioned limit can be up to 85% of the value of your pledged portfolio.

For example: if you pledge mutual fund units worth ₹10 lakh and the applicable LTV is 85%, your sanctioned credit limit will be ₹8.5 lakh. If you draw ₹2 lakh to cover an expense, you will pay interest only on the ₹2 lakh utilized amount, not on the full ₹8.5 lakh limit. The remaining ₹6.5 lakh stays available for withdrawal whenever you need it.

This is the standard structure for most Loan Against Mutual Funds products in India. The terms LAMF and flexi facility against mutual funds are often used interchangeably to describe the same type of product. Your credit limit is determined when you pledge your units and may be reviewed periodically based on changes in the NAV of the underlying mutual funds.

Flexi Loan vs Fixed-Term Loan Against Mutual Funds

Check your credit limit on Volt Money. Free, takes 15 seconds.

Check your limit →

The practical difference comes down to three things: how interest is charged, how repayment works, and what happens when you have extra cash.

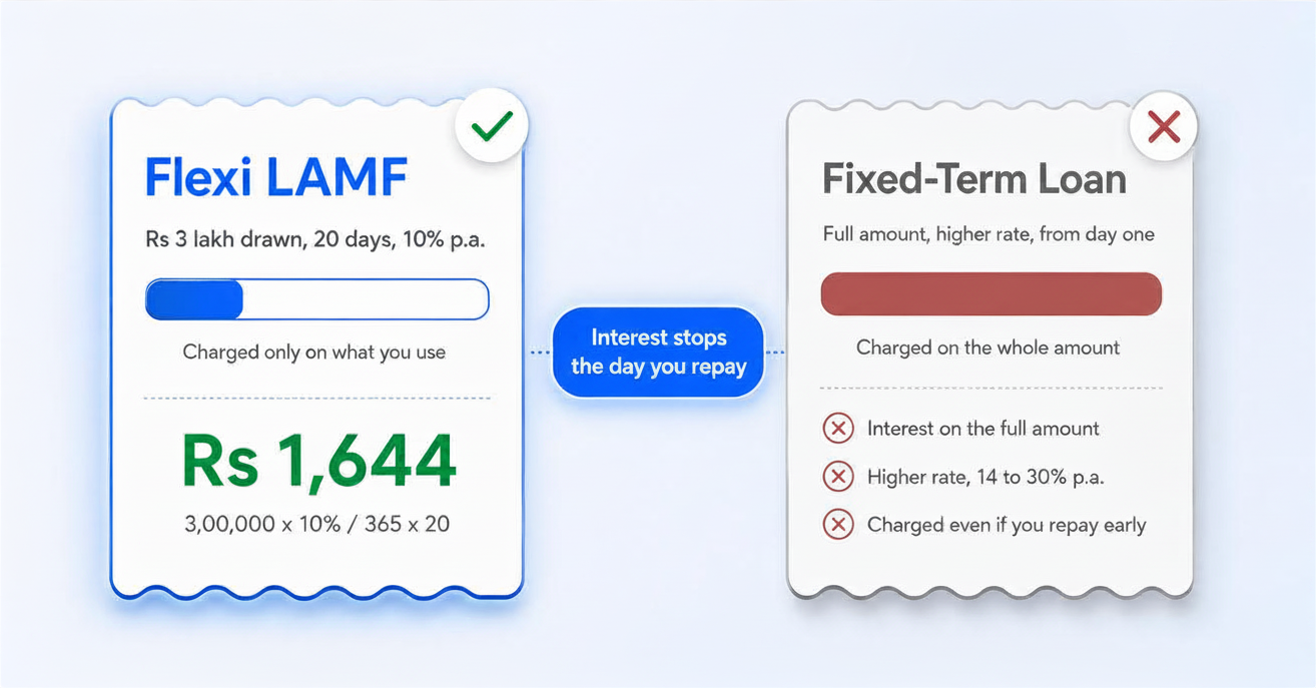

On a flexi facility, interest is calculated daily on the outstanding drawn balance and debited monthly. You pay for exactly the days you hold the balance, on exactly the amount you used. On a fixed-term loan, interest accrues on the full disbursed amount from day one regardless of actual usage.

For example: you draw Rs 2 lakh for 30 days at 10% p.a. — interest is Rs 2,00,000 × 10% / 365 × 30 = Rs 1,644. On a fixed-term loan of Rs 2 lakh at 18% p.a., interest accrues on the full Rs 2 lakh from day one even if you repay in 30 days.

On a flexi facility, there is no fixed repayment schedule. Pay the monthly interest debit and repay principal whenever you have surplus. Every rupee you repay restores your credit limit immediately. A fixed-term loan locks you into principal plus interest payments over a defined tenure.

And on early repayment: a flexi limit costs nothing extra. If you borrow Rs 3 lakh and can repay in 18 days instead of 30, interest stops accruing the day you repay. Most fixed-term loans carry prepayment charges or require you to pay interest for the minimum agreed period.

How Interest Is Calculated on a Flexi Loan Against Mutual Funds

Daily interest formula: Outstanding balance × Annual interest rate / 365.

Example: You draw Rs 3 lakh from a Rs 10 lakh credit facility at 10% per annum. Daily interest = Rs 3,00,000 × 10% / 365 = Rs 82.19 per day. Hold the balance for 20 days and the total interest cost is Rs 1,643.84.

Compare that with drawing the full Rs 3 lakh as a fixed-term loan, where interest accrues on the entire amount for the full tenure regardless of how long you actually need it. With a flexi loan, holding Rs 3 lakh for just 20 days costs only Rs 1,643.84, because interest applies only to the days you hold the balance. And if you only needed Rs 1 lakh of the Rs 3 lakh limit? Your 20-day cost drops to Rs 547.95, since you pay only on what you draw, not on your sanctioned limit.

To estimate before drawing: take your planned withdrawal, multiply by the annual rate, divide by 365, then multiply by the number of days you expect to hold the balance.

Which Mutual Funds Are Eligible for this Facility?

The same rules that apply to standard LAMF apply here. Eligible: equity funds, debt funds (liquid, ultra-short duration, short duration, gilt), hybrid funds, and most ETFs on the lender's approved list. Not eligible: ELSS funds during the 3-year lock-in, closed-end funds within their restriction period, and any scheme outside the approved list.

When a Flexi Product Beats a Fixed-Term Loan

The structure wins whenever your cash need is variable, short-term, or unpredictable.

- Business working capital: Quarterly receipts but monthly expenses? This bridges the gap without charging interest between payment cycles. Draw when you need it, repay when the payment arrives.

- Emergency buffer: A credit limit against your portfolio costs nothing when idle. Keep it open as a low-cost backstop — instant liquidity without holding large amounts in low-yield savings.

- Multiple draws: Three separate needs across a year? A single credit limit handles all three without new applications. Each draw starts its own interest clock independently.

A fixed-term loan makes more sense when you need a large, defined amount for a specific purpose and prefer the discipline of a regular repayment schedule.

Risks of a Loan against Mutual Fund Facility

- NAV-linked limit fluctuations: Your limit is not fixed — it adjusts as portfolio values change. A significant market fall can reduce your available limit without warning, at exactly the moment you might want to draw more. Don't treat the full limit as reliably available.

- Interest accumulation over the tenure: The credit facility runs for up to 6 years. There is no forced monthly principal repayment, so if you only pay the monthly interest without reducing the principal, costs accumulate over time. Set a repayment plan before drawing and treat the outstanding balance as a real liability.

- Margin call in volatile markets: A sharp NAV drop can trigger a margin call. Have a repayment buffer and monitor your portfolio LTV periodically.