When you take a loan against mutual funds, your units are not transferred to the lender. They stay in your name, stay invested, and keep earning returns. What changes is that a lien is placed on them. Lien marking is the mechanism that makes this possible, and understanding it is the key to knowing exactly what happens to your portfolio when you pledge it as collateral.

What Is Lien Marking?

Lien marking is the technical process of recording a pledge at the registrar and transfer agent (RTA) level. In India, mutual fund RTAs are CAMS (serving most fund houses) and KFintech (serving others). When a lender initiates lien marking, the RTA adds a restriction to your unit holdings that prevents any redemption or switch of the specified units.

The lien is specific to a quantity of units, not the full folio. If you hold 1,000 units of an equity fund and only 600 need to be pledged, the remaining 400 units stay fully accessible. You can still redeem those 400 units at any time.

Because LAMF is a credit facility at Volt Money, the lien on your pledged units does not automatically release when you repay. The lien stays active so you can withdraw again any time during your 6-year tenure. When you want to fully exit, request unpledging from the Volt app or website — it completes in under 10 minutes.

What Happens to Your Funds After Lien Marking?

Check your credit limit on Volt Money. Free, takes 15 seconds.

Check your limit →Your pledged units remain in your folio, in your name, accruing NAV growth. The fund continues to send you account statements, dividend credits (where applicable), and NAV updates on lien-marked units in the same way as before.

Your CAMS or KFintech statement will show the lien-marked units separately, typically labelled as 'lien marked' or 'under pledge'. The unrestricted balance in your folio, if any, remains freely available for redemption or switching.

The only restriction is redemption: you cannot sell or switch the lien-marked units until the lien is lifted. This is the core operational constraint to plan around when taking an LAMF.

Which Mutual Funds Can Be Lien-Marked?

Most equity and debt mutual funds can have a lien marked on their units. The key exception is funds under a lock-in period, primarily ELSS funds during the mandatory 3-year lock-in. After the lock-in expires, ELSS units become eligible for pledging like any other equity fund.

Liquid funds, ultra-short-term funds, short-term debt funds, equity funds, balanced funds, hybrid funds, and index funds are all typically eligible. Volt Money accepts more than 9,000 mutual fund schemes for pledging. Your lender's platform will show you which of your specific funds are eligible when you begin the application. For details on locked tax-saving funds, see Loan Against ELSS Mutual Funds.

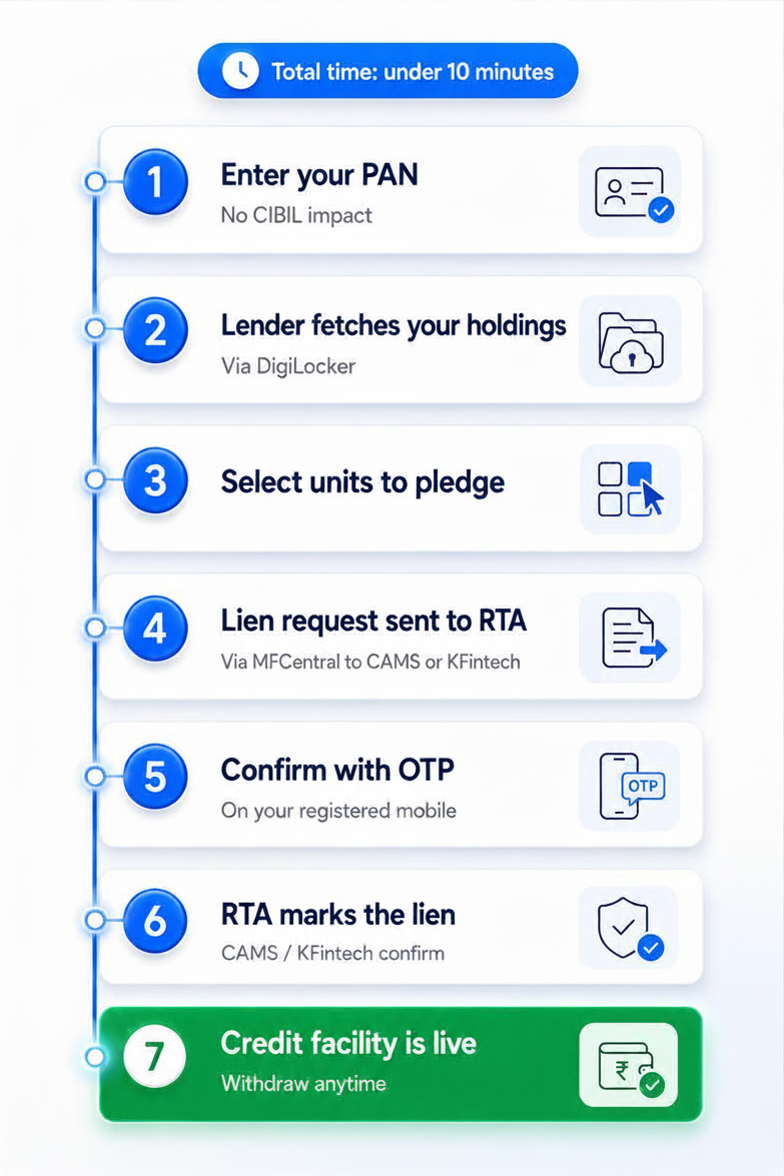

How Lien Marking Works: Step by Step

The process is entirely digital and involves no paperwork:

- You enter your PAN on the lending platform. The lender fetches your KYC details automatically via DigiLocker — no document uploads needed.

- The lender fetches your mutual fund holdings and calculates an eligible credit limit.

- You select the funds and units to pledge as collateral.

- The lender sends a lien marking request to the RTA (CAMS or KFintech) via MFCentral.

- You receive an OTP from the RTA and approve it to confirm the pledge.

- The RTA marks the lien and confirms to the lender.

- The lender activates your credit facility.

Total time from application to active credit facility is typically under 10 minutes. For the complete borrowing walkthrough, see How to Take a Loan Against Mutual Funds.

Lien Marking on MFCentral, CAMS, and KFintech

MFCentral is the central industry platform operated jointly by CAMS and KFintech. Lenders integrated with MFCentral can initiate lien marking across fund houses in one step — the fastest route for most investors and the widest scheme coverage.

CAMS serves fund houses including HDFC MF, ICICI Prudential, Nippon India, and SBI MF. KFintech serves Aditya Birla Sun Life, Kotak MF, UTI MF, and others. Modern LAMF platforms like Volt Money handle both CAMS and KFintech automatically — you do not need to know which RTA manages your funds.

How to Release the Lien When You Repay

At Volt Money, lien release does not happen automatically on repayment. Because LAMF works as a credit facility, the lien remains active after repayment so you can withdraw again. To release the lien on your units, request unpledging from the Volt app or website. Unpledging typically completes in under 10 minutes.

If you are making partial repayments, some lenders allow partial lien releases — units proportional to the repaid amount are freed progressively. This is useful if you want to regain access to part of your portfolio while maintaining the credit facility at a lower amount. Check your lender's specific policy.

Risks of Lien Marking: What to Plan For

- You cannot redeem during a market fall. When markets drop sharply, many investors want to redeem or rebalance. If your units are lien-marked, you cannot act on those units. Plan your pledge amount carefully; keep some portfolio unpledged as a free reserve.

- Margin call risk in a falling market. If NAV drops enough to breach the LTV threshold, you must pledge more units or repay. Borrow conservatively: keep your drawn amount well below the full credit limit to create a buffer.

For the broader picture across asset classes, see Loan Against Securities.