The interest rate on a loan against securities determines how much your borrowed money actually costs, and the difference between a well-chosen secured product and a personal loan can be substantial. LAS rates in India range from around 9.99% for fund-backed credit facilities to over 15% for some stock-backed products from smaller NBFCs. Most personal loans start at 12% and commonly reach 22% to 24%, so LAS borrowers can save up to 30% or more on interest. Here is how rates are structured, what drives them, and how to calculate your actual cost before committing.

Current LAS Interest Rates in India (2026)

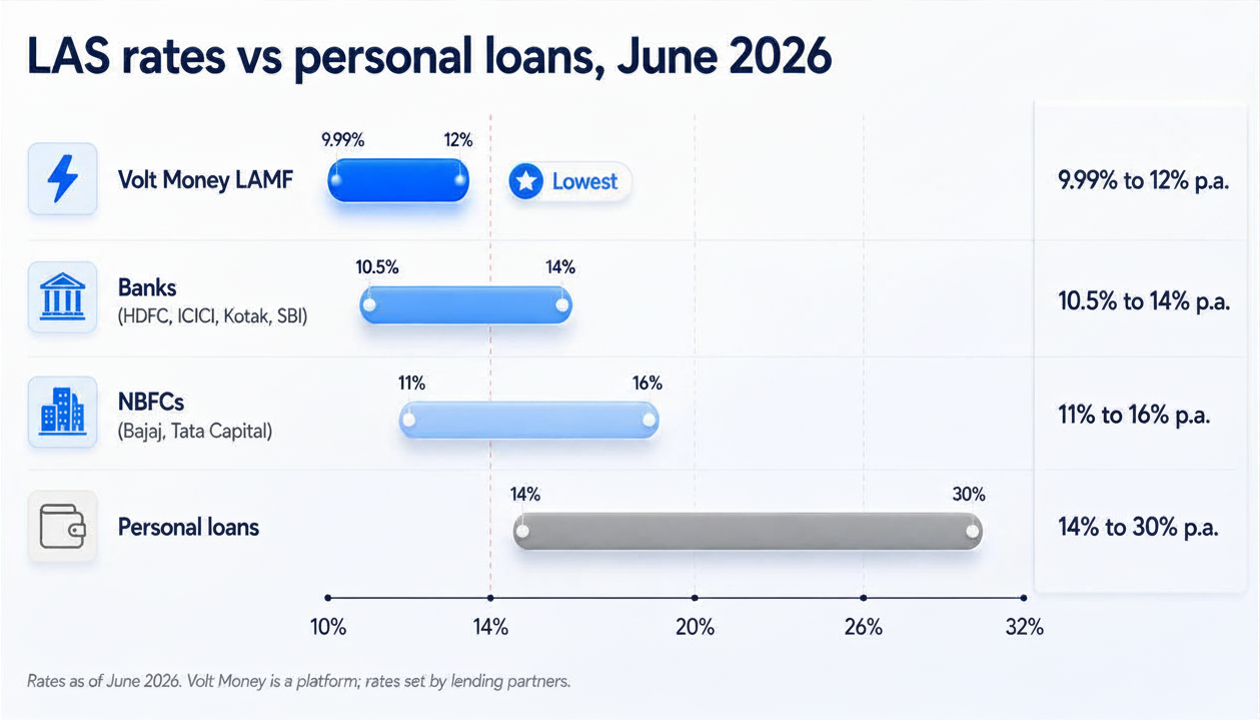

LAS interest rates vary by lender type, collateral, and loan size. Current benchmarks for 2026 are shown in the table below. Rates are sourced from publicly available lender rate sheets, including ICICI Bank's official LAS interest rate page, which lists rates for individual accounts opened in Q4 FY 2025–2026, as well as published rates from Volt Money, Bajaj Finserv, and Tata Capital. For broader NBFC rate context, Bankopedia's 2026 guide on loans against mutual funds notes that rates across lenders typically range from 9% to 13% p.a. for equity fund pledges, with NBFCs generally charging a bit more than banks.

| Lender Type | Collateral | Rate (2026) |

|---|---|---|

| Dedicated LAMF platforms (e.g. Volt Money) | Mutual fund units | 9.99% to 12% p.a. |

| NBFCs (e.g. Bajaj Finserv, Tata Capital) | Stocks, bonds, MF | 10.5% to 16% p.a. |

| Banks (e.g. HDFC, ICICI, Kotak, SBI) | Equity credit facilities | MCLR/repo-linked; ~10.5% to 14% |

All LAS products are structurally cheaper than unsecured alternatives. A personal loan from the same bank or NBFC typically starts 3 to 5 percentage points higher than their LAS product — the security reduces the lender's risk, and that saving is passed on to the borrower.

How LAS Interest Rates Are Determined

Check your credit limit on Volt Money. Free, takes 15 seconds.

Check your limit →Two factors primarily drive LAS rates: collateral quality and the lender's cost of funds.

Collateral quality is the bigger driver. Mutual funds are highly liquid and transparent — a liquid debt fund can be redeemed in one day. A small-cap stock might have limited daily trading volume and sharp price swings. Lenders reflect this difference directly in the rate they charge, which is why LAMF rates are structurally lower than stock-backed LAS rates.

Cost of funds determines the floor. Banks borrow at the repo rate or MCLR, while NBFCs borrow from markets at higher rates. Bank LAS products are often cheaper than NBFC products for the same collateral, though banks have stricter eligibility criteria and slower processes.

Banks vs NBFCs vs Fintech Platforms: Rate Comparison

| Lender | Examples | Rate Range | Collateral |

|---|---|---|---|

| LAMF platforms | Volt Money (in partnership with its Lenders) | From 9.99% p.a. | Mutual fund units |

| Banks | HDFC, ICICI, Kotak, SBI | ~10.5% to 14% p.a. | Equity (MCLR/repo-linked) |

| NBFCs | Bajaj Finserv, Tata Capital, Zerodha Capital | ~11% to 16% p.a. | Stocks, bonds, MF units |

Fixed vs Floating Rates on LAS

Most LAS products carry floating rates linked to the lender's benchmark (MCLR, external benchmark, or repo rate). If the RBI cuts the repo rate, a repo-linked LAS rate may fall. If MCLR rises, an MCLR-linked LAS rate rises with it.

Fixed-rate LAS products exist but are less common. They offer predictability — you know exactly what you will pay for the duration. Fixed rates are typically slightly higher than the starting floating rate to compensate for certainty.

For short-term borrowing under 90 days, the rate type matters less because the benchmark is unlikely to change significantly in that window. For loans held over 6 to 12 months, a floating rate in a falling interest rate environment works in your favour.

LAS vs Personal Loan: A Real Cost Comparison

You borrow Rs 5 lakh for 90 days. At 10% p.a. (LAS, mutual fund-backed): Interest = Rs 5,00,000 × 10% × 90/365 = Rs 12,329. At 18% p.a. (personal loan, typical mid-range): Interest = Rs 5,00,000 × 18% × 90/365 = Rs 22,192.

The saving on a single 90-day drawdown is nearly Rs 10,000. On a larger amount or longer tenure, this compounds quickly. Beyond the rate, LAS typically carries no processing fee for drawdown, while personal loans levy 1% to 3% upfront. On Rs 5 lakh, that is another Rs 5,000 to Rs 15,000 in upfront cost that LAS avoids.

How to Calculate Your Total LAS Interest Cost

Formula: Principal Drawn × (Annual Rate / 100) × (Days Outstanding / 365).

Example: Rs 3 lakh drawn for 45 days at 10% p.a. = Rs 3,00,000 × 0.10 × 45/365 = Rs 3,699.

If you make a partial repayment midway, interest is computed only on the remaining balance for the remaining days. This is the fundamental cost advantage of a credit facility over a fixed-term loan, and why LAS almost always costs less for variable or uncertain cash needs.

Tips to Get a Lower Rate on Your LAS

- Use mutual funds as collateral where possible. LAMF rates are structurally lower than stock-backed LAS rates. Even if you hold both, pledging MF holdings first gives you the lower rate.

- Choose debt or liquid funds as primary collateral when eligible. Debt funds attract higher LTV and sometimes lower rates than equity funds.

- Compare total cost, not just the rate. Include processing fees, prepayment charges (usually nil for LAS), and any annual maintenance fees. A lower headline rate with a 2% processing fee can end up more expensive than a slightly higher rate with no fee.

For the full picture, see Loan Against Securities: Complete Guide and Zerodha Loan Against Securities.