Indian investors tend to think of loans in one of two ways: personal loans or home loans. But if you hold stocks, bonds, or mutual funds, there is a third option that most people overlook. A loan against securities (LAS) lets you pledge financial assets to unlock a credit limit without selling them. Your investments keep compounding. You pay interest only on what you actually use.

What Is a Loan Against Securities (LAS)?

A loan against securities is a credit facility where you pledge eligible financial assets — such as stocks, mutual funds, government bonds, or ETFs — with a lender. The lender creates a lien on those assets and releases a credit facility, usually 40% to 90% of the current market value depending on the asset type. Debt mutual funds attract up to 85% to 90% LTV, while equity-backed products typically range from 50% to 70%.

You do not sell your investments. They remain in your portfolio and continue to generate returns. If you hold equity funds that appreciate while your loan is running, you benefit from both the capital growth and the liquidity from the credit facility simultaneously.

LAS is sometimes called loan against shares when the collateral is primarily listed equities, or loan against mutual funds (LAMF) when the collateral is mutual fund units specifically. The underlying mechanics are similar — pledge your assets, create a lien, draw funds as needed, repay at your pace. The flexi structure means that as you repay, the credit refills and you can draw again.

Types of Securities You Can Pledge for LAS

Check your credit limit on Volt Money. Free, takes 15 seconds.

Check your limit →The range of eligible securities is wider than most investors expect. Accepted collateral types typically include:

- Listed equity shares (NSE/BSE listed, subject to the lender's approved list)

- Equity and debt mutual funds (regular and direct plans, subject to scheme eligibility)

- Government securities and RBI bonds

- Exchange-traded funds (ETFs) including gold ETFs and index ETFs

- Non-convertible debentures (NCDs) and sovereign gold bonds with select lenders

The exact list varies by lender. Dedicated LAMF platforms like Volt Money work with lenders whose approved securities lists cover over 9,000 mutual fund schemes — one of the broader eligible lists available for MF-backed lending in India.

How LAS Works: Pledge and Lien Marking

LAS has two stages: pledge creation and fund drawdown.

For mutual funds, pledge creation happens through your registrar and transfer agent (RTA). The lender sends a request to mark a lien on specified units. The RTA marks the lien, and those units cannot be redeemed, switched, or transferred until the lien is released. No ownership transfer occurs. The units remain in your folio, in your name, earning returns.

For listed shares, the pledge creation involves your demat account. Your demat holdings are pledged through CDSL or NSDL via your broker, which requires signing physical or broker-assisted documentation.

Once the pledge is confirmed, the lender creates a credit limit. You draw as needed and pay interest only on what you have withdrawn. The full mechanics of the mutual fund pledge process — how lien marking works across MFCentral, CAMS, and KFintech — are covered in detail in What Is Lien Marking on Mutual Funds.

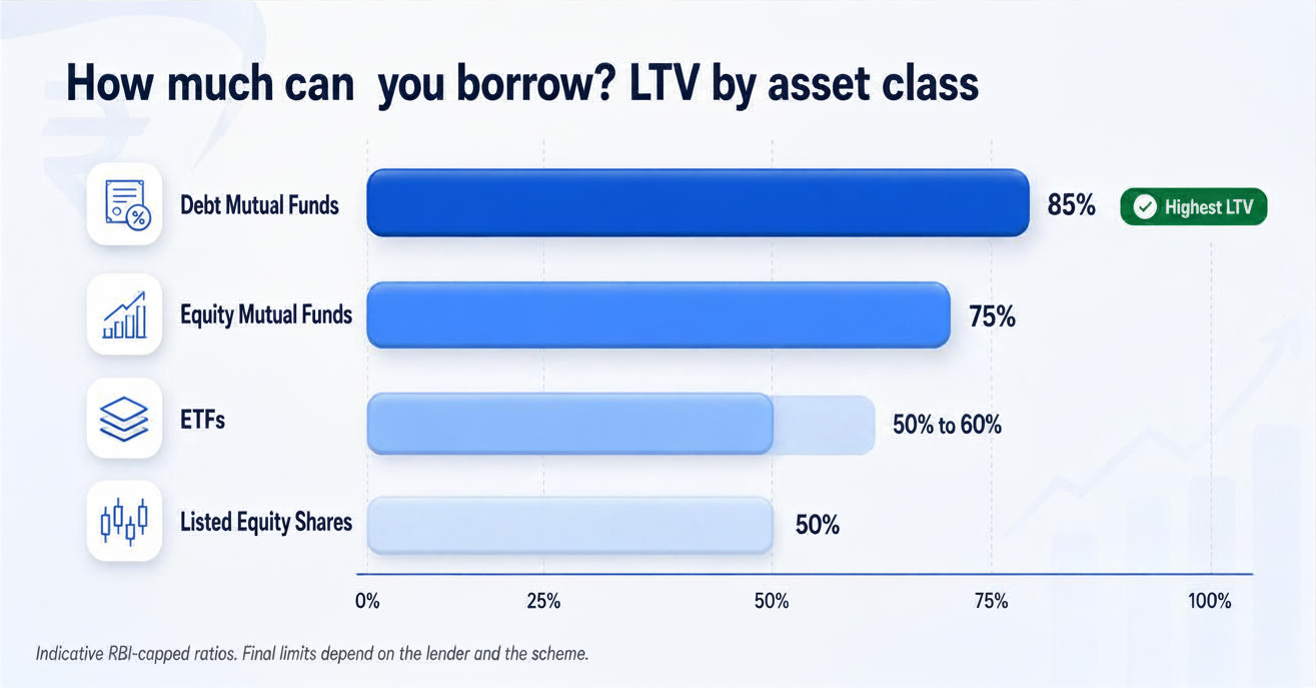

Loan-to-Value (LTV) Ratios by Asset Class

LTV is the percentage of your asset's market value you can borrow. RBI regulations prescribe maximum LTV caps for loans against securities:

- Equity mutual funds: up to 75% LTV

- Debt mutual funds: up to 85% LTV

- Listed equities (individual stocks): up to 50% LTV

- ETFs: up to 50% to 60% LTV depending on the underlying composition

If your equity mutual fund portfolio is worth Rs 10 lakh at 70% LTV, your credit limit is Rs 7 lakh. If the NAV of those funds falls and your LTV rises above the threshold, the lender will ask you to pledge additional units or repay part of the outstanding balance.

LAS vs Loan Against Mutual Funds: Key Differences

Both allow you to unlock liquidity without selling. The practical difference is in collateral scope and the process.

LAS covers the broadest collateral base — stocks, bonds, ETFs, and mutual funds. If your portfolio has all of these, a full LAS product from a bank or broker can potentially lend against the whole thing. LAMF is a subset of LAS specifically for mutual fund units, with a more streamlined lien-marking process via MFCentral, CAMS, and KFintech.

For investors whose wealth is primarily in mutual funds, a dedicated LAMF platform like Volt Money typically offers competitive rates and faster end-to-end processing. And if part of your wealth is in shares, you no longer need to go to a bank or broker: Volt Money now also offers loans against shares, with loans against demat mutual funds coming soon, making it a single platform for all your loan-against-securities needs.

LAS Interest Rates in India (2026)

LAS rates vary by lender type and collateral. As a working benchmark for 2026: dedicated LAMF platforms start at 9.99% p.a. for mutual fund collateral; NBFCs typically charge 10.5% to 16% for stock-backed LAS; banks offer repo-linked or MCLR-linked rates, generally 10.5% to 14% for equity-backed LAS.

For a detailed rate comparison across specific banks, NBFCs, and platforms, and to see how rates are determined, see Loan Against Securities Interest Rates in India 2026.

Eligibility and Documents Required

Eligibility for LAS is generally clear: Indian resident above 18 years, a qualifying financial portfolio meeting the minimum value threshold, and KYC compliance with a valid PAN and Aadhaar/other OVD. No minimum credit score is required for most MF-backed loans.

For most modern platforms, the entire process is digital with just OTP verification — no physical documents or branch visits required.

Risks: Margin Call, NAV Drop, Forced Liquidation

Margin call is the main risk to manage. If the value of your pledged securities falls below the LTV threshold, the lender issues a margin call: pledge more securities, make a partial repayment, or face liquidation. For stock-backed LAS, this risk is acute — a 20% fall in a pledged stock can breach the LTV within a single trading session. Mutual fund-backed LAMF carries lower margin call risk because NAVs move more gradually.

Forced liquidation: if you cannot meet a margin call in the specified window (typically within 7 working days), the lender will sell pledged securities to restore the required LTV. This may lock in losses at the worst possible time.

LAS does not make sense when your pledged securities are highly volatile, or when you are borrowing close to the maximum LTV. For investors whose wealth is primarily in mutual funds, see What Is a Loan Against Mutual Funds.